While the COVID-19 pandemic is finally slowing down, the economic damage that it caused lingers on. In order to relieve the financial burdens facing many taxpayers and accelerate recovery, Congress has passed the American Rescue Plan Act (the Act). The Act is a $1.9 trillion relief package that will affect millions of individuals and businesses.

A summary of the Act’s key tax provisions follows.

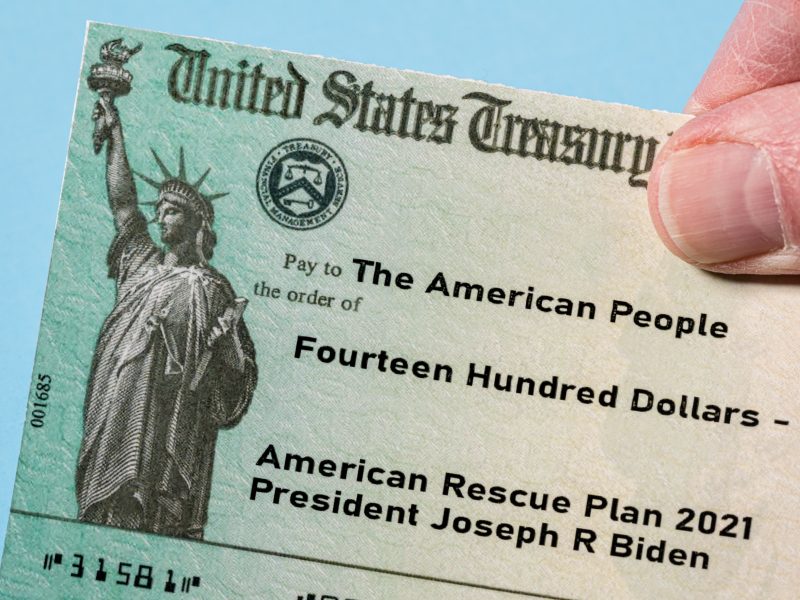

Direct Payments

$1,400 stimulus checks for individuals ($2,800 in the case of joint returns and $1,400 for dependents) to be phased out for individuals with adjusted gross income of $75,000 – $80,000 ($150,000 – $160,000 for married filing jointly and $112,500 – $120,000 for head of household).

Extension of Unemployment Insurance

The Act extends two COVID-19 related unemployment insurance programs to allow unemployed individuals to receive, or continue receiving, $300 per week of unemployment insurance payments. These payments, which were scheduled to expire on March 14, 2021, will continue until September 6, 2021, and are in addition to any state unemployment benefits for which an individual may qualify.

Portion of Unemployment Insurance May Be Excludible from Income

For 2020 only, up to $10,200 (or $20,400 in the case of a joint return where each spouse receives unemployment compensation) may be excludible from income to the extent an individual’s adjusted gross income is less than $150,000.

Expansion of Child Tax Credit

Under the Act, the child tax credit is increased from $2,000 to $3,000 or, for children under 6, to $3,600; the age at which a child is eligible for the child tax credit is increased from 16 years old to 17 years old; the refundable amount of the credit is increased so that it equals the entire credit amount, rather than having the taxpayer calculate the refundable amount based on an earned income formula; and monthly payments of the credit are available for the last six months of 2021.

Increase in Earned Income Credit (EITC)

The Act nearly triples the amount of the EITC available for workers without qualifying children; it expands the eligible age range for individuals who qualify for the EITC; it increases the amount of investment income an individual can have before being ineligible for the EITC; and a special rule for 2021 expands the eligibility and amount of the EITC for taxpayers with no qualifying children.

Increase in Dependent Care Assistance Tax Benefits

The Act makes the child and dependent care tax credit refundable; increases the amount of expenses eligible for the credit; increases the maximum rate of the credit; increases the applicable percentage of expenses eligible for the credit; and increases the exclusion from income for employer-provided dependent care assistance.

Expansion of the Affordable Care Act Subsidies

The Act provides a two-year temporary subsidy to individuals who buy health insurance under the Patient Protection and Affordable Care Act (PPACA) resulting in drastic reductions in health care costs for such individuals. The Act also eliminates the income cap on who is eligible for PPACA healthcare subsidies and reduces the cost of health insurance by limiting premiums to, at most, 8.5 percent of income.

Assistance with COBRA Premiums

The Act assists individuals with COBRA premiums (i.e., premiums paid to continue insurance coverage after leaving employment with a employer that had been providing health insurance coverage) by providing that the government will pay for COBRA premiums through September of 2021.

Modification of Student Loan Forgiveness

The Act excludes certain discharges of student loan debt occurring in years 2021 through 2025 from gross income.

Extension of Refundable Payroll Tax Credits for Employers and Self-Employed Individuals

The Act extends the refundable payroll tax credits for paid sick time and paid family leave through September 2021.

Extension of Employee Retention Credit for Employers Subject to Closure as a Result of COVID-19

The Act allows as a credit against applicable employment taxes for each calendar quarter an amount equal to 70 percent of qualified wages of up to $10,000 for each calendar quarter. Additionally, a credit of up to $50,000 is available for a recovery startup business for any calendar quarter. A recovery startup business is one which was started after February 15, 2020, had receipts of less than $1 million and meets certain other requirements.

Extension of Deductibility of Excess Farm Losses and Excess Business Losses

The Act allows taxpayers other than corporations to deduct excess farm losses and excess business losses through 2027, instead of through 2026;

Modification of Exceptions for Reporting of Third Party Network Transactions

The Act lowers the threshold for the amount of sales that will cause a payment processor to send a Form 1099K to a seller. Previously, the threshold was $20,000 in gross receipts when collected in over 200 transactions. After 2021, that threshold is $600.

Preferential Treatment of EIDL and Restaurant Revitalization Grants

The Act provides that these grants are not includible in the recipient’s income.

Because of the extent of this legislation, it may be helpful for us to meet at your convenience to discuss the ramifications of the Act’s various provisions on your tax situation.

IRS Statement – American Rescue Plan Act of 2021

IRS Statement – American Rescue Plan Act of 2021

Leave a Reply